> For the complete documentation index, see [llms.txt](https://docs.kasu.finance/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://docs.kasu.finance/how-kasu-works/lending-strategies-explained/whole-ledger-funding-professional-services-firms/technology-driven-risk-management-and-security-structuring.md).

# Technology-Driven Risk Management & Security Structuring

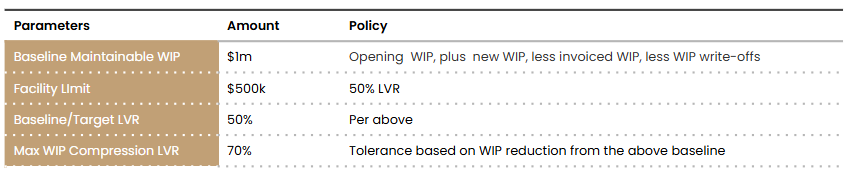

### Work-in-Progress (**WIP) Funding**

A credit due diligence process is undertaken in order to establish a WIP funding limit. This process determines a firm’s ‘baseline’ maintainable WIP on a ‘normalised’ basis. Once the baseline WIP is sized, 50% LVR (for Accounting Firms) or 40% LVR (for Law Firms) is applied to establish the facility limit. In the case of WIP compression (reduction) from the baseline, LVR cannot exceed 70% (Accounting Firms) or 60% (Law Firms). Notwithstanding the LVR increase associated with WIP compression, funding cannot exceed the established facility limit. The process is summarised as follows:

1. Apxium provides a portal through which firms upload their monthly WIP.

2. Detailed commentary must be provided, itemising WIP movement and breakdown, such as opening/carried over WIP (from the previous month), new WIP, less invoiced WIP, less WIP ‘write-offs.’ This establishes a month end adjusted WIP amount upon which funding is advanced.

3. Should WIP compress from the ‘baseline,’ then a revised funding amount for the month will be the lower of:

1. 70% LVR (Accounting Firms) / 60% LVR (Law Firms) of the reduced WIP; or,

2. The approved facility limit, being 50% LVR (Accounting Firms) / 40% (Law Firms) of the baseline maintainable WIP.

4. The firm must open a new Collateral & Fees bank account (which Apxium will impose a minimum cash balance covenant based on a Firm’s weighted average invoice size) to effect an automated chargeback via Apxium’s direct debit authority in the case of the following triggers:

1. The revised funding amount for the month (caused by the above) is to reduce; and/or,

2. Should WIP recede to a level where LVR exceeds 70%.

The above process occurs on a 90-day rollover period basis. Fees are charged on the basis of a flat percentage rate every quarter (90 days), payable in advance upon each drawdown. The worst case WIP advance rates (70% and 60% LVR for Accounting and Law Firms respectively) are based on Apxium’s experience with these borrowers’ worst case WIP recovery rates.

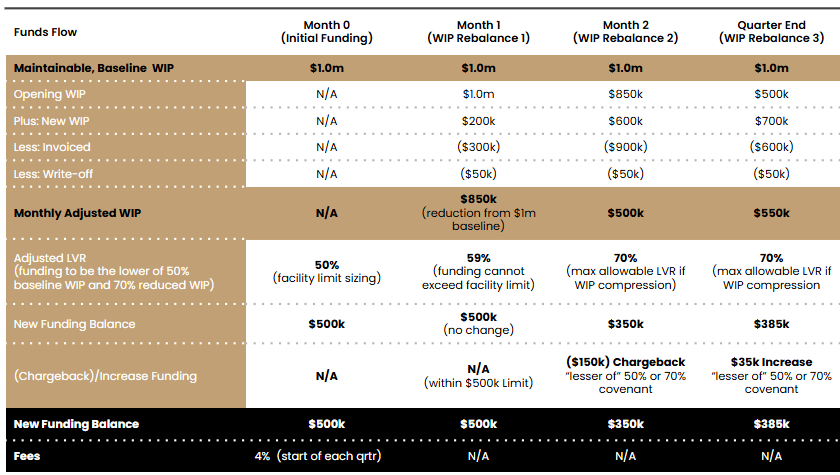

### WIP Funding Example - Accounting Firm

### **Receivables Funding**

Apxium’s Payments Acquiring accreditation means it replaces each Firm’s transactional banking relationship (i.e. Apxium offers the same payment rails as banks, but in a smarter and more cost effective manner, that is fully data integrated with firms’ Practice Management Software). Combined with innovative Accounts Receivable Automation software, Apxium acts as the Firm’s Collections Agent, which is managed per the following funds flow explanation

The diagram reveals a simple example of how Apxium’s AR Automation Software and Payment Rails delivers a seamless Receivables Funding solution with superior risk management. The example assumes a $1,000 invoice upon which 100% LVR is extended. For simplicity, although Whole Ledger Funding also enables firms to fund WIP, this is a Receivables funding example only.

It is noted that each Firm is required to also operate a Collateral & Fees Bank Account, with a minimum cash balance covenant to ensure adequate liquidity to fund interest, fees and chargebacks associated with any funded invoices that exceed 120 days. The minimum cash balance covenant will be based on the firm’s weighted average invoice amount. Some firms will have access to this account completely restricted.

**Step 1** demonstrates how Apxium’s AR software automates the invoice presentment process to the Firm’s client. In this example, the firm offers its client 30 day terms to pay the $1,000 invoice per Step 2.

**Step 3** assumes the Firm opts to finance the $1,000 invoice, with funds settled to its Collections Account. This would incur a 2% fee upfront, debited to the Firm’s Collateral & Fees account. **Steps 4-5** assume the invoice is paid by the firm’s client on day 30 (therefore, no additional fees are charged to the firm).

Should the Firm’s client not pay upon the due date, the following incremental fees apply (deducted from the invoice payment proceeds: 31-60 days, +1% fee; 61-90 days, +2% fee; 91-120 days, 3%. Upon day 121, a chargeback will occur to the Firm’s bank account, with an additional 3.5% fee. Repayment occurs via an automated cash sweep of the Collections account via Apxium’s Direct Debit Authority.

The security structure per Step 6 reveals how Apxium can effect an automated cash chargeback to the Firm’s Collateral & Fees account for any outstanding invoices over 120 days. A chargeback will also be effected in the case that the Firm manually adjusts its Receivables ledger associated with any credit notes, reversals, cash payments etc. Apxium’s data integration and synchronisation technology with firms’ Practice Management Software ensures it can recognise such adjustments to the Receivables ledger in real time.

Although a minimum cash balance covenant is imposed on the Collateral & Fees account, should the cash chargeback exceed the available cash balance (dishonour), Apxium also has the ability exercise a ‘Right of Offset’ to route all invoice payments to Apxium, even for invoices that have not been funded. This is made possible by the Condition Precedent that the firm must utilise Apxium’s AR Automation Software and Payment Rails, which manages all invoices and collections (funded and unfunded). In the unlikely event that the firm faces insolvency, Apxium has also the ‘Right to Perfect Title’ from the firm’s end debtors for any unpaid invoices.

Whole Ledger Funding - Credit Risk Structuring

It is a condition precedent that the Firm will always be a user of Apxium’s Accounts Receivable Automation Software and Payment Rails. The Firm will have also executed the Facility Agreement providing Apxium with the right to auto Direct Debit the Firm’s bank accounts for the full amount of debt outstanding in relation to any defaults (i.e. 120+ days outstanding invoices or excess WIP beyond the LVR covenant). Prior to any such Direct Debit being actioned for a Receivables related chargeback, Apxium will inform the firm that: 1) its client has failed to meet its obligations; 2) is in default; and, 3) that the firm will be immediately debited for the amount outstanding.\

\

In the event of a chargeback/reimbursement, Apxium’s Accounts Receivable Automation Software will still assist the Firm to collect these monies owed to it. It is ultimately the Firm’s responsibility to collect funds owed (given the loan amount has already been repaid by the firm to Apxium by this time). If the Direct Debit on the Firm’s account fails, Apxium has the additional protection to ‘offset’ the amount owed against settlements that are due to the firm via Apxium’s main Accounts Receivable Automation system activities. This Right of Offset is also included in the Facility Agreement. Such an ‘offset’ would be notified formally in writing to the firm.

Apxium’s existing Professional Fee Funding (PFF) loan portfolio has never suffered a loss in its entire 8 years of existence. Whilst Whole Ledger Funding differs in the firm’s ability to access funding against its WIP and Receivables, Apxium’s proven security structure associated with PFF will be largely replicated.

Apxium’s Payments Acquiring accreditation and Payment Retails means it replaces each Firm’s transactional banking relationship (i.e. Apxium offers the same payment rails as banks, but in a smarter and more cost effective manner, that is fully data integrated with Firms’ Practice Management Software). This ensures a deep level of control over all debtor collections, where when combined with the AR software’s management of all invoices, Apxium is able to trigger automated backstops to mitigate default and arrears risk. The following comprehensive process demonstrates multiple risk ‘back-stops’ to mitigate losses.

#### **Backstop 1** **- Automated Cash Sweep**

Apxium holds Direct Debit Authority over each firm’s Collections Bank Account to which all invoices are paid. This enables Apxium to effect an automated cash sweep to immediately repay each funded invoice in full.

#### **Backstop 2** - Automated Chargeback

An automated chargeback event (via Apxium’s Direct Debit Authority) occurs upon day 121 for any funded invoices that are yet to be repaid, thereby reimbursing Apxium for the full outstanding amount of the invoice. A Collateral & Fees Bank Account is established, with a minimum cash balance covenant in line with the firm's weighted average invoice value. This minimum cash balance covenant aims to mitigate dishonours. It is also noted that interest and fees are also debited to this account. Automated chargebacks are also affected in the case that WIP exceeds the LVR covenant.

Depending upon each Firm’s credit quality, some firms will not have access to the Collateral & Fees account to which chargebacks are effected. Importantly, via Apxium, all parties have real-time visibility as to late debtor/invoice payments. The firm will therefore have ample opportunity to contact its defaulting client debtor and establish if the payment arrears is capable of being remedied.

#### **Backstop 3** - Right of Offset

In the event that a chargeback amount exceeds the cash balance of the Collateral & Fees account, Apxium will exercise its ‘Right of Offset.’ Given that it is a Condition Precedent that every borrower must utilise Apxium’s AR Automation Software and Payment Rails, this ensures that Apxium not only has real time visibility over every invoice and debtor collection (payment), but it also provides the ability to access all collections (even for invoices that haven’t even been funded). Apxium is therefore able to route all debtor collections to itself until debts are fully paid. This is also made possible by Apxium’s Equitable Assignment over the firm’s Receivables Ledger.

#### Backstop 4 - Right to Perfect Title

In order for all the above backstops to fail, this would assume that the firm is in financial stress and unable to meet its obligations. Should this worst case scenario eventuate, Apxium’s Right to Perfect Title provides an additional mechanism through which it can pursue the firm’s client debtor for any unpaid invoices.

#### Backstop 5 - Guarantee & Indemnity over the Firm

This enables Apxium to activate its Enforcement & Step-in Rights.

#### Backstop 6 - Personal Guarantees given by Partners/Directors and/or Beneficial Owners

This added security layer deems the firm’s partners personally liable for debt owed in the event that all other ‘backstops’ fail.

Given the above, Apxium therefore operates a unique ‘multi-recourse’ security structure over both the Firm, its Partners and its client debtors. Given Apxium’s ability to auto Direct Debit the Firm’s bank accounts to recover any monies owed, along with a full Right of Offset for all invoice payments that haven’t even been financed (as Apxium manages all the firm’s accounts receivable collections) the Firm would have to face insolvency (as a worst case scenario) before Apxium suffers any losses. Therefore, in the event that Apxium has exhausted all reimbursement protocols from both the firm, its partners and its client(s), any recoveries would be subject to a formal administration process (in a worst case scenario). Apxium is a secured creditor of the accounting firm via its security position/structure.

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter, and the optional `goal` query parameter:

```

GET https://docs.kasu.finance/how-kasu-works/lending-strategies-explained/whole-ledger-funding-professional-services-firms/technology-driven-risk-management-and-security-structuring.md?ask=&goal=

```

`ask` is the immediate question: it should be specific, self-contained, and written in natural language.

`goal` is optional and describes the broader end goal you are ultimately trying to accomplish on behalf of the user. GitBook uses it to tailor the answer towards what is most useful for that goal.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.